Introduction

As the world’s largest production and consumption hub for polypropylene, fluctuations in China’s PP market prices deeply impact the global plastics supply chain. Since 2026, driven by geopolitical conflicts, cost-push factors, and supply contractions, the price center for PP has shifted significantly upward. However, supply-demand contradictions and forward-looking pressures remain non-negligible. Based on the latest market data, this article provides a professional analysis for global industry practitioners.

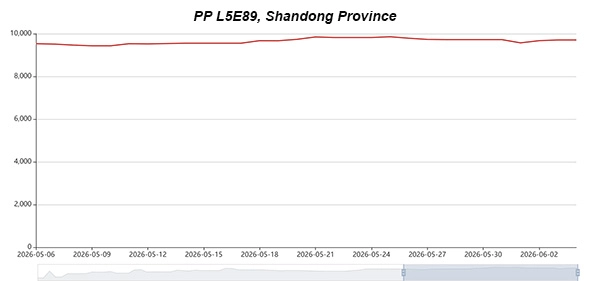

Price Overview: High-Level Operation with Basis Hitting a Near Six-Year High

In 2026, the Chinese PP market demonstrated a pattern of opening high and fluctuating. As of June 5, spot quotes for raffia PP stood at approximately 9,800 RMB/ton in East China, 9,900 RMB/ton in South China, and 9,550 RMB/ton in North China. The active main PP futures contract closed at 8,683 RMB/ton (data as of June 4), pushing the basis past 1,000 RMB/ton to a near six-year high, highlighting a tug-of-war characterized by a “strong spot market vs. weak futures market.”

In terms of specific grades, raffia prices recently surpassed low-melt copolymer, with the price spread briefly reaching -200 RMB/ton, primarily driven by reduced raffia production scheduling and concentrated export orders.

Supply Side: Maintenance Wave Contracts Spot Supply, Operating Rates Drop to Historical Lows

Short-term supply tightness is the core driver of current high prices. In May, the domestic PP industry experienced its largest wave of turnarounds in recent years, pulling the industry-wide operating rate down to 62%–64%, a year-on-year drop of about 13 percentage points. Performance varied significantly across different production pathways:

| Production Pathway | Operating Rate | Underlying Cause |

| Coal-to-PP (CTP) | 90%–95% | Manageable and stable coal costs |

| Oil-to-PP | 59.42% | High crude prices leading to losses and load reductions |

| PDH-to-PP | 52.50% | Soaring propane prices resulting in deep financial losses |

Cumulative maintenance-induced volume losses from January to April reached 3.78 million tons, representing a sharp year-on-year surge of 62.35%. As of June 3, port inventories fell by 3.64% month-on-month, keeping the overall supply chain running on low inventory levels.

Cost Side: Coal Pathway Thrives While Oil and PDH Suffer Deep Losses

Geopolitical conflicts have driven up feedstock prices. From January to May 2026, the average cost for oil-to-PP stood at 8,634 RMB/ton, while PDH-to-PP costs soared to 9,679 RMB/ton, representing year-on-year increases of 11.8% and 18.9%, respectively. Thanks to stable domestic coal prices, coal-to-PP demonstrated a prominent cost advantage, making it the only pathway to maintain strong margins (with profits exceeding 1,000 RMB/ton). Conversely, oil-to-PP and PDH-to-PP suffered losses ranging from 500 to 1,500 RMB/ton, rendering cost support a rigid floor for PP prices.

Demand Side: Weak Domestic Demand Offset by Explosive Export Growth

Downstream operating rates remained generally sluggish, averaging just 47.7%, as high resin costs suppressed procurement appetites. However, exports emerged as the biggest highlight: PP export volume in April skyrocketed to 639,400 tons, a month-on-month jump of 57.7% and a year-on-year surge of 123.6%. China is shifting from a net importer to a net exporter; this massive release of export volume has effectively relieved domestic inventory pressures and supported high-level PP price operations.

Short-Term Outlook: Strong Reality Sustains, But Forward Pressures Accumulate

- Short-Term (June–July): As offline plants have not yet fully restarted and inventories remain low, spot availability will stay tight, keeping prices supported by both costs and supply. However, the gradual conclusion of spring maintenance and a marginal deceleration in export growth will cap further upside potential.

- Medium-to-Long Term (H2): The third quarter will witness a concentrated rollout of new capacities exceeding 3 million tons, making oversupply pressures unavoidable. If geopolitical tensions ease and feedstock supplies normalize, the price center faces a substantial downside correction risk.

Conclusion

The Chinese PP market currently resides in a critical transition phase of “strong reality vs. weak expectations.” While the spot market shows short-term strength, forward capacity expansions pose the primary downside risk. Global supply chain participants should closely monitor maintenance dynamics, the sustainability of export volumes, and the actual implementation schedule of new production capacities.