As a core engineering plastic for automotive, electrical & electronics, and industrial manufacturing industries, PA66 exhibits highly interconnected global pricing dynamics. Combining the latest spot market and foreign trade transaction data for June 2026, this article provides a comprehensive analysis of the volatility logic behind global and Chinese PA66 spot prices, alongside a short-term market forecast, serving as a professional reference for global resin procurement and foreign trade ordering.

Current Global & Chinese PA66 Spot Transaction Prices (Mid-June 2026 Real-Time Quotations)

The prices listed below reflect the average tax-inclusive / FOB transaction prices of mainstream general-purpose prime PA66 chips on the market. These do not include special modifications, flame-retardant, or medical-grade customized formulations, and are uniformly benchmarked against the industry-standard EPR27 general-purpose grade.

Chinese Market Spot Prices

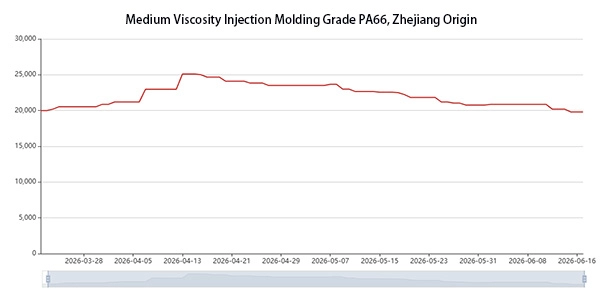

- Mainstream General-Purpose PA66 Chips in East China: The current transaction range stands at 19,500–20,200 RMB/ton. Throughout June, the price fell by 4.65% month-on-month compared to May, with the market continuing its correction from high levels. Ex-factory prices from domestic integrated adiponitrile plants have been adjusted downward simultaneously, and the industry operating rate remains at 60%–63%, ensuring an ample supply of goods.

- China Export FOB Prices: The mainstream FOB quotation for Southeast Asia ranges between 2,180–2,250 USD/ton. Its distinct price advantage makes it the core procurement source for small and medium-sized processing plants in Southeast Asia.

Overseas Regional Spot Prices

- Europe BASF / Radici General-Purpose PA66 Spot Price: 2,850–2,980 USD/ton, under slight downward pressure.

- North America Ascend / Invista Domestic Spot Price: 2,700–2,820 USD/ton, showing stable supply and demand, with a smaller decline than that observed in the Asian market.

- Southeast Asia CIF Price: 2,350–2,430 USD/ton, fully correlating with fluctuations in Chinese supply, lagging behind the Chinese market trend by 3–7 days.

Core Driving Factors behind the Current PA66 Price Fluctuations

Synthesizing the current state of the supply chain fundamentals, this round of global PA66 weakness is driven primarily by three core factors, with no unexpected unilateral bullish triggers present:

Weakening Cost Support from Upstream Raw Materials

International Brent crude oil has pulled back below 80 USD/barrel, causing the prices of raw materials like pure benzene and butadiene to decline. Concurrently, new domestic adiponitrile and hexamethylenediamine capacities in China have achieved stable production, pushing raw material self-sufficiency rates higher. Lacking any upward momentum, upstream raw materials have completely undercut the cost support for PA66, expanding the pricing leeway for manufacturers.

Continual Weakness in Downstream Terminal Demand

The global automotive industry has entered its mid-year procurement off-season, resulting in limited order growth for electric vehicle (EV) battery-motor-electronic control systems and internal combustion engine (ICE) structural components. Downstream tire cord fabric sectors are displaying strong resistance to high prices. Consequently, global processing plants have uniformly adopted a hand-to-mouth procurement model focused on small, immediate-need orders, with an extremely low willingness to stock up in bulk. This sluggish market activity has failed to support resin prices.

Structural Loosening of Global Supply and Demand

The continuous release of integrated PA66 production capacity in China has led to a clear domestic oversupply situation, fostering a strong desire to push sales through exports. In Europe and North America, leading facilities have completed their maintenance turnarounds and returned to full-capacity operations. As a result, the global availability of general-purpose PA66 chips is highly abundant, leaving the overall supply and demand fundamentals weak.

Short-Term (July 2026) PA66 Market Forecast

Overall Conclusion: Global prices will fluctuate weakly, with limited room for further steep declines and divergent regional performances.

Chinese Market: The market is expected to maintain a narrow, weak consolidation pattern. General-purpose chips in East China will fluctuate within a range of 19,200–20,000 RMB/ton, with declines narrowing. The bottom-level pricing of hexamethylenediamine will restrict deep downward movements. Export FOB prices will remain stable, facilitating foreign trade order transactions.

European & American Markets: Prices will experience minor adjustments, with volatility remaining lower than that in Asia. Quotations will hold around 2,800–2,950 USD/ton, showing stronger downward resistance backed by domestic automotive replacement and baseline demand.

Southeast Asian Market: Prices will edge downward slightly in tandem with Chinese cargo movements. The CIF spread will remain stable, and procurement focuses will continue shifting toward high-cost-performance, Chinese-made PA66.

Key Takeaways for Global Procurement

- Clear Price Advantage: Currently, Chinese FOB supply is 500–650 USD/ton lower than European and American domestic supply. For general-purpose structural components, tire cord fabrics, and standard injection-molded parts, priority should be given to Chinese domestic supply to compress procurement costs.

- Inventory Pacing Recommendation: The market is currently sitting within a mid-year low price window. Overseas buyers can opt to lock in volumes via long-term contracts in batches, mitigating the risk of purchasing at higher prices should a minor seasonal rebound occur in late July.

- Quality Differentiation Reminder: While general-purpose chips are experiencing a noticeable price decline, specialized PA66 grades—such as glass fiber reinforced, hydrolysis-resistant, and high-temperature modified types—maintain independent price stability without synchronous drops. Premium grades still command original factory premiums from European and American manufacturers.

High-Frequency FAQs for Foreign Trade Customers

Q1: Is the current stage suitable for bulk hoarding of PA66?

A: It is suitable for moderate, staggered restocking in batches, but full-capacity hoarding is discouraged. While current prices hover at the low end of the second quarter, suggesting minimal further downside, downstream off-season demand has not rebounded, indicating a lack of near-term surges. Locking in contract volumes dynamically in batches will satisfy immediate manufacturing needs while avoiding capital tie-ups.

Q2: Does Chinese PA66 currently possess complete environmental and export compliance certifications?

A: Yes. General-purpose PA66 from leading integrated Chinese enterprises complies fully with EU RoHS and REACH environmental standards, and conventional grades carry UL certifications. There are no export trade barriers, and zero export tariffs apply to basic chips, ensuring smooth foreign trade customs clearance.

Q3: Can PA6 be used to replace PA66 during the off-season to lower production costs?

A: This substitution is feasible only for low-load, civil-use components. PA6 possesses weaker heat resistance, rigidity, and oil resistance compared to PA66. Therefore, replacement is impossible for high-voltage automotive components, tire cord fabrics, and high-temperature electrical accessories. However, low-end applications like basic cable ties and minor outer housings can temporarily pivot to PA6 for cost-control purposes.

Disclaimer

The pricing, supply, and demand data cited in this article are derived from public industry databases including IHS Markit, CCF Global, and SunSirs. They are intended solely for market analysis and procurement reference and do not constitute any spot transaction or futures investment advice. Actual transaction prices may vary depending on order volumes, logistics terms, and customized grades; final execution prices shall be subject to real-time quotations from original factories and distributors.