Current Market Price Levels

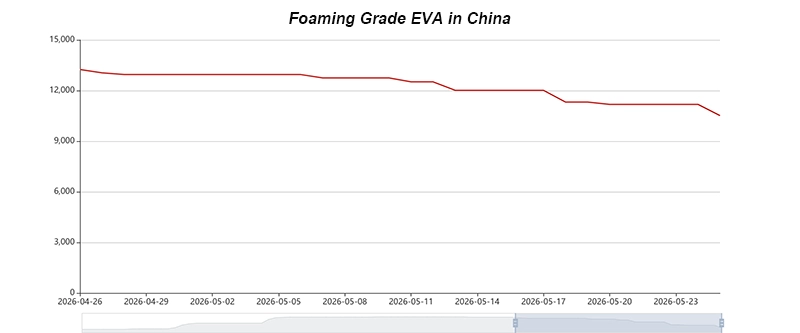

As of May 26, 2026, the benchmark price for ethylene-vinyl acetate (EVA) copolymer in the Chinese market stands at 10,516.67 RMB/ton. This represents an 18.79% decline compared to the 12,950 RMB/ton recorded at the beginning of May, with a single-day drop of 5.96%. The current price resides within the mid-to-low range of the past 12 months.

Since mid-May, EVA prices have entered an accelerated downward channel. By May 14, the benchmark price had fallen to 12,016 RMB/ton, down 7.21% from the start of the month. In the final week of May, prices for both foaming-grade and photovoltaic (PV) grade EVA continued to edge lower, accompanied by thin overall market trading.

Key Turning Points in Recent Price Fluctuations

On May 25, 2026, several mainstream EVA producers centralized reductions in their ex-factory quotes:

- Yangzi-BASF lowered its V5110J grade by 700 RMB/ton, down to 10,350 RMB/ton.

- Sinopec Yangzi Petrochemical reduced its 2825DV listing price by 1,000 RMB/ton, down to 12,000 RMB/ton.

- Jiangsu Sailboat Petrochemical significantly slashed its UE2806 grade by 3,000 RMB/ton, down to 10,500 RMB/ton.

These price adjustments directed a distinctly bearish guidance onto the spot market. Meanwhile, Jiangsu Hongjing New Material raised its ex-factory price by 500 RMB/ton to 14,000 RMB/ton, indicating that select enterprises still maintain an intention to prop up prices. Overall, the recovery of downstream demand remains sluggish, and bearish sentiment dominates the market, leaving short-term prices under evident pressure.

Price Trend Review (January–April): Policy-Driven Impulse Rally

In the first quarter of 2026, the Chinese EVA market experienced a round of rapid upward price action driven by policy expectations, supply contractions, and escalating costs. By April 13, the benchmark price climbed to 13,350 RMB/ton, marking a 36.69% surge from the 9,766 RMB/ton seen at the start of the year.

Primary Drivers of the Price Increase:

- The “Last Train” Effect of the PV Export Tax Rebate Policy: Effective April 1, China eliminated export tax rebates for photovoltaic products. From late March through April, PV module manufacturers centralized aggressive export shipments, triggering emergency restocking by PV encapsulant film factories. Because EVA used for PV film accounts for 50%–60% of total EVA demand, this short-term demand surge disrupted the supply-demand balance.

- Concentrated Supply-Side Turnarounds: During the second quarter, Chinese EVA production units entered a wave of centralized maintenance turnarounds exceeding the scale of previous years, leading to a phased reduction in output throughout April and May. Concurrently, geopolitical factors closed the import arbitrage window, causing year-on-year import volumes to plummet by over 50% and tightening spot availability.

- Substantial Inflation of Raw Material Costs: By April 13, the price of ethylene (Sinopec East China) rose to 9,800 RMB/ton, up 62.4% from the beginning of the year. Meanwhile, vinyl acetate monomer (VAM) in the East China market climbed to 12,300 RMB/ton, a 34.5% increase from the year’s opening. Surging crude oil prices pushed feedstock costs upward, prompting producers to repeatedly raise ex-factory quotes and further reinforcing bullish market sentiment.

Moving into late April, the market trend shifted from a rally to a correction. Although plant maintenance significantly lowered monthly production volumes, downstream factory orders contracted, resulting in insufficient demand recovery. Downstream resistance toward high-priced inventory became pronounced, causing transactions to steadily weaken.

Core Drivers of the Current Price Downturn

1. Weakening Demand-Side Support The PV sector, as the largest consumer of EVA (accounting for 50%–60% of Chinese EVA consumption), has seen a noticeable deceleration in its purchasing rhythm. Following the closure of the tax rebate policy window, export orders for module enterprises retreated, reducing the procurement appetite of film factories, which have shifted to consuming existing inventories. Concurrently, the traditional application sector—foaming footwear—has entered its off-season, acting as a drag on EVA prices.

2. Persistent Supply Pressure Although a few production lines remain under maintenance in May, previously shut-down units are steadily restarting, causing market supply volumes to gradually recover. China’s total EVA capacity reached 3.8 million tons/year by the end of 2025, a 35.7% increase compared to 2024. For 2026, an additional 1.69 million tons/year of new capacity is planned for launch, meaning medium-to-long-term oversupply pressures remain unabated.

3. Market Sentiment Shifting to Pessimism The centralized reduction of ex-factory prices by production enterprises shattered previous expectations of price support. Traders and downstream users have adopted a wait-and-see posture, limiting procurement to small, rigid-demand orders. The market lacks any incentive to hoard stock, leaving prices without the support needed for a rebound.

Short-Term and Medium-Term Outlook

Short-Term (Next 2–4 Weeks): EVA prices are highly likely to extend their weak, corrective adjustments. Downstream PV film enterprises are operating at capacity rates of only 50%–60%, with slow follow-through on new orders; seasonal demand in traditional sectors like footwear is also turning weaker. Technically, the moving average system exhibits a bearish alignment, indicating potential for further downward price testing. However, considering that some producers have already slipped into losses or razor-thin margins, and that feedstock costs (ethylene, VAM) have not experienced a synchronous steep decline, the room for further deep drops remains limited. The short-term price range is projected to fluctuate between 10,000 and 11,500 RMB/ton.

Key Focus Areas for Global Buyers

For international buyers sourcing EVA from China, the current market delivers several vital takeaways:

- Prices Are at a Relative Low: The current price of around 10,500 RMB/ton represents a low level not seen since the fourth quarter of 2025, making it an opportune time for buyers with immediate needs to build positions in batches.

- Abundant Supply Options: Sourcing origins in the Chinese EVA market are highly diversified, featuring stable supplies of PV-grade, foaming-grade, and cable-grade products from enterprises such as Jiangsu Sailboat, Zhejiang Petrochemical, Shaanxi Yanchang Petroleum (Yanchang Energy Chemical), and Gulei Petrochemical.

- Export Window Opportunities: Driven by continuous domestic capacity expansion and intensified domestic competition, Chinese enterprises possess a heightened willingness to export. In 2025, China’s EVA export volume reached approximately 309,000 tons, a year-on-year increase of 22%, with Southeast Asia, South Asia, and the Middle East serving as primary destinations. The weakening of current Chinese domestic prices may further widen the export arbitrage window.

- Quality and Certification: Major Chinese EVA suppliers have obtained international certifications including ISO, REACH, and RoHS, with PV-grade products fully satisfying the technical specification requirements of downstream encapsulant film factories.